What is the Asia Pacific Photoresist and Photoresist Ancillaries Market Overview – Definition, scope, and significance?

The Asia Pacific Photoresist and Photoresist Ancillaries Market encompasses the production, distribution, and application of photoresist materials and supporting chemicals used in photolithography processes across semiconductor, LCD, and printed circuit board manufacturing. Photoresists are light‑sensitive polymers that define circuit patterns, while ancillaries such as anti‑reflective coatings, removers, and developers enable precise pattern transfer and defect control. This market is vital for the region’s rapidly expanding semiconductor ecosystem, underpinning advanced node development and the broader electronics supply chain.

What are the key drivers, restraints, challenges, and opportunities shaping the Asia Pacific Photoresist and Photoresist Ancillaries Market?

Primary drivers include the surge in demand for high‑performance chips in smartphones, data centers, and automotive electronics, along with aggressive technology roadmaps targeting sub‑5 nm nodes. Government initiatives and substantial capex in fabs across China, South Korea, and Taiwan further fuel growth. Restraints arise from stringent environmental regulations on chemical handling and the high cost of next‑generation photoresist formulations. Challenges involve supply‑chain fragility and the need for continuous innovation to meet shrinking feature sizes. Opportunities stem from emerging applications such as 3‑D IC stacking, EUV lithography adoption, and the growth of flexible display manufacturing, which require specialty resists and ancillary solutions.

What are the current growth trends in the Asia Pacific Photoresist and Photoresist Ancillaries Market?

Trend analysis shows a clear shift toward extreme ultraviolet (EUV) compatible resists, especially ArF immersion and dry photoresists, as manufacturers target advanced nodes. Parallelly, there is increasing adoption of KrF and G‑line/I‑line resists for mature‑node production, supporting cost‑effective volume manufacturing. Developers are also focusing on low‑toxicity ancillaries to comply with sustainability standards. The market is witnessing consolidation through strategic alliances between resist manufacturers and equipment suppliers, accelerating technology transfer and market penetration.

How did COVID‑19 impact the Asia Pacific Photoresist and Photoresist Ancillaries Market and what is the recovery trajectory?

The pandemic initially disrupted supply chains, causing temporary shortages of raw materials and delayed fab expansions. However, the rapid rebound in demand for consumer electronics and data‑center infrastructure mitigated the impact. Recovery accelerated in late 2021, with fabs ramping up capacity and resuming postponed projects. The market has since entered a growth phase, supported by pent‑up demand and accelerated digital transformation, positioning it for sustained expansion.

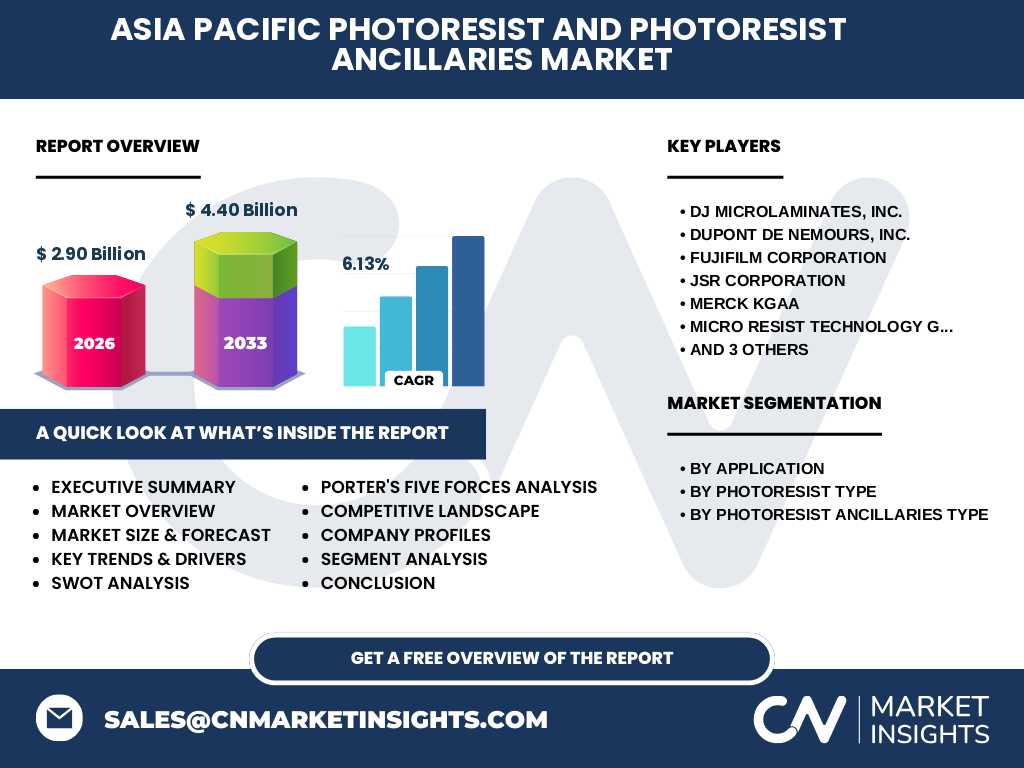

Who are the major competitors in the Asia Pacific Photoresist and Photoresist Ancillaries Market and what does the competitive landscape look like?

The competitive arena is dominated by well‑established chemical and materials corporations such as DJ Microlaminates, Inc., DuPont de Nemours, Inc., Fujifilm Corporation, JSR Corporation, MERCK KGaA, Micro Resist Technology GmbH, Shin‑Etsu Chemical Co., Ltd., Sumitomo Chemical Co., Ltd., and TOKYO OHKA KOGYO CO., LTD. These players compete on product performance, portfolio breadth, and customer support. Recent years have seen strategic collaborations and acquisitions aimed at consolidating technology expertise and expanding geographic reach within the Asia Pacific region.

What are the key findings presented in the Executive Summary of the Asia Pacific Photoresist and Photoresist Ancillaries Market?

The executive summary highlights a market size of USD 2.90 billion in 2026, projected to reach USD 4.40 billion by 2033, representing a compound annual growth rate (CAGR) of 6.13 %. Growth is driven by advanced node demand, EUV adoption, and expanding applications in LCD and PCB sectors. The region’s leading players are intensifying R&D investments and forming alliances to address supply‑chain resilience and sustainability challenges, positioning the market for robust upside potential.

What are the forecast expectations for the Asia Pacific Photoresist and Photoresist Ancillaries Market from 2025 to 2032?

Forecast modeling indicates a steady upward trajectory, with the market expanding from its 2026 baseline of USD 2.90 billion to approximately USD 4.40 billion by 2033. This reflects the 6.13 % CAGR, driven by continued fab capacity additions, the transition to EUV lithography, and the diversification of end‑use applications such as flexible displays and advanced packaging. The outlook suggests strong demand for both high‑performance resists and ancillary chemicals that support next‑generation manufacturing processes.

How is the Asia Pacific Photoresist and Photoresist Ancillaries Market sized and shared by segmentation?

By application, the market is divided among semiconductors and integrated circuits (ICs), liquid‑crystal displays (LCDs), and printed circuit boards (PCBs), each requiring distinct resist formulations. By photoresist type, the segments include ArF immersion photoresist, ArF dry photoresist, KrF photoresist, and G‑line/I‑line photoresist, reflecting varying wavelength requirements. Ancillary types are categorized as anti‑reflective coatings, removers, and developers, which together enable the complete lithographic workflow. While specific numeric shares are not disclosed, the semiconductor segment commands the largest portion due to its high volume and technology intensity.

What is the global Asia Pacific Photoresist and Photoresist Ancillaries Market size and share by region?

The Asia Pacific region accounts for the majority of the global market, driven by the concentration of leading semiconductor fabs in China, Taiwan, South Korea, and Japan. This geographic dominance reflects both the manufacturing footprint and the strategic investments made by governments and private enterprises to boost domestic chip production. The region’s share underscores its pivotal role in supplying photoresist and ancillary products to worldwide customers.

What does the regional analysis reveal about the performance of the Asia Pacific Photoresist and Photoresist Ancillaries Market?

Country‑level analysis shows China as the fastest‑growing market, propelled by its “Made in China 2025” policy and aggressive fab construction. Taiwan maintains a strong position due to its mature foundry ecosystem, while South Korea benefits from leading memory and logic manufacturers. Japan contributes robust R&D capabilities and high‑value ancillary production. Collectively, these sub‑regions exhibit complementary strengths—capacity expansion, process innovation, and specialty chemical expertise—that drive overall regional growth.

Which companies are leading in the Asia Pacific Photoresist and Photoresist Ancillaries Market and what are their strategic approaches?

Key players such as DuPont and Fujifilm focus on high‑performance EUV‑compatible resist lines, leveraging extensive IP portfolios. JSR and Shin‑Etsu prioritize cost‑effective solutions for mature nodes, catering to volume PCB and LCD manufacturers. MERCK and Micro Resist Technology emphasize specialty chemicals for niche applications, while Sumitomo and TOKYO OHKA expand their ancillary portfolios through partnerships with equipment vendors. These strategies reflect a balance between catering to advanced‑node demand and sustaining mature‑node market share.

How does Porter’s Five Forces framework apply to the Asia Pacific Photoresist and Photoresist Ancillaries Market?

Threat of new entrants is moderate due to high R&D costs and stringent regulatory barriers. Bargaining power of suppliers is limited, as raw material sources are diversified, though specialty chemical components can be concentrated. Bargaining power of buyers is significant, with major fabs demanding customized performance and volume discounts. Threat of substitutes remains low, as alternative lithography chemistries are not yet commercially viable. Industry rivalry is intense, driven by product differentiation, technological leadership, and strategic alliances.

What are the SWOT elements for the Asia Pacific Photoresist and Photoresist Ancillaries Market?

Strengths: Established supplier base, advanced R&D capabilities, and strong alignment with semiconductor roadmaps. Weaknesses: High development costs and sensitivity to raw‑material price fluctuations. Opportunities: EUV lithography expansion, growth in flexible displays, and increasing demand for sustainable ancillaries. Threats: Regulatory tightening, supply‑chain disruptions, and rapid technology cycles that may render existing formulations obsolete.

What does the value chain analysis reveal about the Asia Pacific Photoresist and Photoresist Ancillaries Market?

The value chain begins with raw‑material suppliers (organic monomers, solvents), proceeds to formulation and synthesis by photoresist manufacturers, followed by rigorous testing and qualification for specific lithography tools. Distribution channels include specialized chemical distributors and direct supply agreements with fabs. End‑users—foundries and IDMs—integrate the resists and ancillaries into their process flows, providing feedback that drives iterative product improvements. Collaboration at each stage is critical for maintaining yield and performance.

What key investment insights can be drawn for stakeholders in the Asia Pacific Photoresist and Photoresist Ancillaries Market?

Investors should target companies with diversified portfolios covering both EUV‑ready and mature‑node resists, as this balances growth and revenue stability. Funding R&D initiatives focused on low‑toxicity ancillaries aligns with sustainability trends and regulatory expectations. Strategic stakes in firms forging partnerships with leading equipment manufacturers can accelerate market entry. Additionally, monitoring government‑backed fab projects provides insight into future demand spikes across the region.

What are the main conclusions and takeaways from the Asia Pacific Photoresist and Photoresist Ancillaries Market analysis?

The market is on a clear growth path, projected to expand to USD 4.40 billion by 2033 at a 6.13 % CAGR. Demand is anchored by advanced semiconductor node development, EUV adoption, and the diversification of display and PCB applications. Competitive dynamics emphasize innovation, sustainability, and strategic collaborations. Companies that can deliver high‑performance, environmentally compliant solutions while navigating supply‑chain complexities are positioned to capture the most value.

What research methodology was employed to compile this market report?

The study utilized a mixed‑method approach, combining primary interviews with industry executives, technical experts, and supply‑chain participants, alongside secondary data collection from company reports, regulatory filings, and reputable market databases. Quantitative modeling applied historical growth rates and forward‑looking forecasts, calibrated to the provided market size of USD 2.90 billion in 2026 and the projected USD 4.40 billion in 2033, yielding the 6.13 % CAGR. Qualitative insights were validated through cross‑checking with multiple sources.

What is the scope of this research and its limitations?

The scope covers the Asia Pacific region, focusing on photoresist materials and ancillary chemicals across semiconductor, LCD, and PCB applications. Segmentation includes photoresist type, ancillary type, and end‑use application. Limitations arise from the confidentiality of certain proprietary data, which restricts the disclosure of exact market shares for individual segments and companies. Nonetheless, the analysis provides a comprehensive view of trends, drivers, and competitive dynamics.

Which key companies are highlighted and what recent developments have they announced?

Highlighted firms include DJ Microlaminates, Inc., which recently launched an EUV‑compatible low‑k resist; DuPont de Nemours, Inc., announcing a partnership with a major foundry to co‑develop next‑generation immersion resists; Fujifilm Corporation, unveiling a new line of eco‑friendly developers; JSR Corporation, reporting capacity expansion in its Korean plant; MERCK KGaA, introducing a high‑resolution anti‑reflective coating; Micro Resist Technology GmbH, securing a supply agreement for KrF resists; Shin‑Etsu Chemical Co., Ltd., launching a G‑line resist optimized for 28 nm; Sumitomo Chemical Co., Ltd., acquiring a niche remover technology; and TOKYO OHKA KOGYO CO., LTD., partnering with a PCB manufacturer to supply customized developer solutions. These developments underscore ongoing innovation and strategic positioning within the market.